Why Fraud Is Changing — and What the Smartest Banks Are Doing About It

Fraud has gone digital — from fake IDs to AI-generated paystubs and synthetic identities costing U.S. lenders billions. Discover how top banks fight back. DeepXL’s real-time fraud defense, forensic document checks, and explainable AI helps building trust — and keeps money — safe.

THE EVOLUTION OF THEFT

In the past, fraudsters had to rob a bank to steal money.

Today, they just need a laptop, a few stolen files — and a convincing story.

As financial institutions move faster and rely more on automation, fraud has evolved into a silent, digital epidemic. It hides in applications, documents, and even customer interactions — and the price tag keeps climbing.

At DeepXL, we talk to lenders and banks every week who are seeing the same pattern:

fraud is no longer about “if” — it’s about where it’s hiding this time.

Let’s look at the three biggest fraud challenges shaking up the U.S. lending and banking industry right now — and what’s being done to fight back.

1. The Ghost Borrower: Synthetic Identity Fraud

Imagine someone who doesn’t exist — but still has a credit score, a driver’s license, and even a car loan.

That’s synthetic identity fraud in action.

Fraudsters combine real and fake data (like a stolen Social Security number mixed with a made-up name and address) to create entirely new “people.” These identities are then used to apply for loans, credit cards, and buy-now-pay-later accounts — often slipping through traditional verification systems.

According to TransUnion, synthetic identity exposure has reached over $3 billion in the U.S. lending market, and it’s rising fast.

Why is it so hard to stop?

Because synthetics look real — they build credit histories over time, pass basic KYC checks, and behave just like legitimate customers until they vanish.

The new defense: modern verification tools now combine data enrichment, behavioral signals, and forensic checks on submitted IDs to spot inconsistencies invisible to the human eye. Real-time AI models can compare metadata, fonts, and structural markers across thousands of documents — instantly catching forgeries before they reach approval.

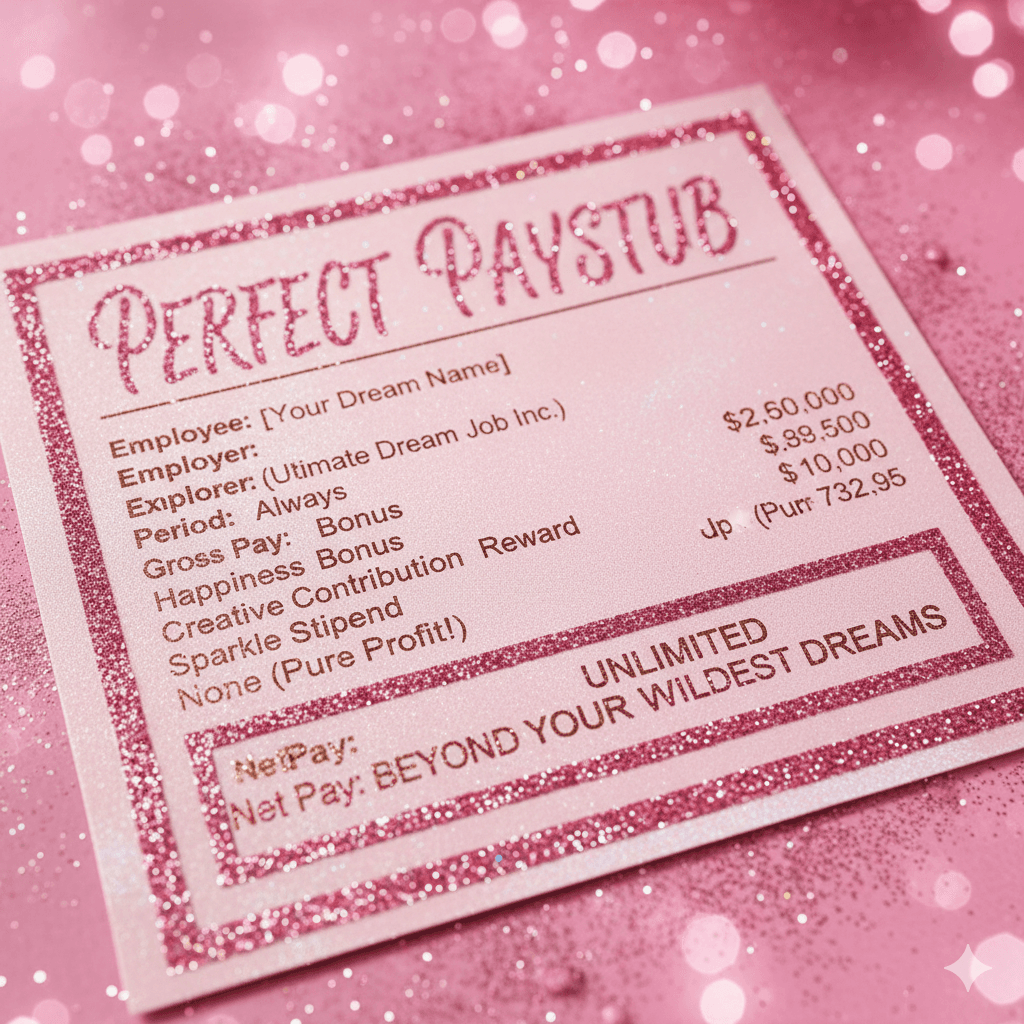

2. The Perfect Paystub: Document Fraud

If you’ve ever looked at a paystub or bank statement and thought, “That looks fine,” you’re not alone. Underwriters see hundreds of these every day — and fraudsters know exactly how to exploit that.

Today, fake paystubs, forged PDFs, and edited bank statements are flooding loan applications. Many are generated using AI tools that replicate real document templates with scary accuracy.

In auto and consumer lending, document fraud has become one of the most expensive forms of first-party fraud, driving billions in annual losses.

A single fake paystub can lead to a bad loan, which turns into a charge-off, which then ripples through portfolios and risk models. The damage isn’t just financial — it affects trust, compliance, and reputation.

The new defense: forensic document analysis. By looking beneath the surface — fonts, pixel-level artifacts, metadata, structure, and even copy-paste traces — lenders can now identify when a file has been altered, reused, or synthetically created. And when the system can explain why it made that decision, compliance teams get a clear audit trail, not just a red flag.

3. The Stolen Account: Payment & APP Fraud

Even when onboarding is secure, fraud can strike later.

Account takeovers (ATOs) and authorized push payment (APP) scams are exploding — especially across instant payment networks like Zelle or RTP.

Criminals gain access through stolen credentials or social engineering. Sometimes they don’t even hack the system — they simply trick the user into authorizing a transfer. Once the money moves, it’s gone.

Banks face not only financial loss but also rising pressure from regulators and customers demanding reimbursement. The CFPB has already warned that institutions must do more to protect users on instant payment rails.

The new defense: layered identity checks, behavioral analytics, and re-authentication at critical moments. By verifying not just who someone was when they opened an account, but who they are when they transact, banks can catch anomalies in real time.

The Bigger Picture: Trust Is the Real Currency

All three fraud types share one thing in common — they exploit trust.

Trust in documents. Trust in data. Trust in digital identity.

That’s why the next generation of fraud defense isn’t just about blocking attacks — it’s about making verification transparent, explainable, and scalable.

At DeepXL, we believe fraud prevention should feel like an invisible layer — built into every onboarding flow and transaction, helping lenders make faster, safer decisions without disrupting the customer experience. Like Stripe did for payments, we’re doing for fraud defense.